Recent selling has been relentless, with the S&P 500 index down -8.7% since the start of October, and about flat for the year. The index remains on track for its worst month since 2010. Global equities (US and international) have lost almost $8 trillion of value this month, and is set to be the biggest wipe-out since the height of the financial crisis a decade ago.

A bear market is defined by most as a decline in equities of -20% or more. Many are asking, are we heading into a bear market?

If I knew the answer to this question, I would be Nostradamus! Everyone wants to know the answer to this question, and for all the punditry and prognostications in the media (what I call “noise”), no one knows.

There are many explanations for the potential causes of the stock market’s recent decline: the economic woes in China and other international markets; the adverse effect of a stronger US dollar; tariff issues; increases in raw material prices (for example, oil); political uncertainty (a looming US mid-term election); increasing inflation; rising interest rates; and profit margin pressures.

But, ultimately, all of these factors feed into the one thing that matters most for stock market returns: earnings growth.

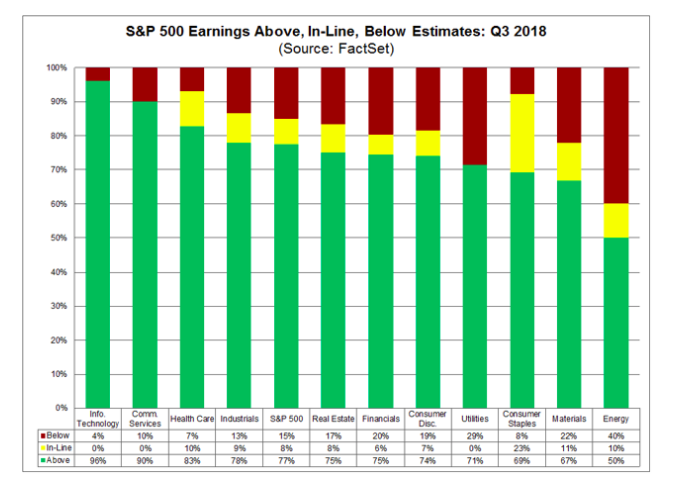

Earnings for Q3 (third quarter) continued to show strength. In fact, 77% of companies have reported Earnings Per Share (EPS) above the five-year average. The chart below from FactSet illustrates EPS by sector. The green shows the percentage of companies in the S&P 500 Index whose earnings came in above estimates. As you can see, technology and consumer services have so far been the big winners.

While earnings growth appears solid, the stock market is forward-looking, and over the past month, it has been forecasting a potential slow-down in earnings growth. But again, corporate earnings are outside of your control.

So, what can you do to weather a potential bear market?

Are your investments appropriate for you? Know yourself… and your appetite for risk.

The truth is that an individual’s investment experience comes primarily down to human behavior and emotions. It’s true for most everyone – even portfolio managers – which is why a disciplined, data-driven approach is important.

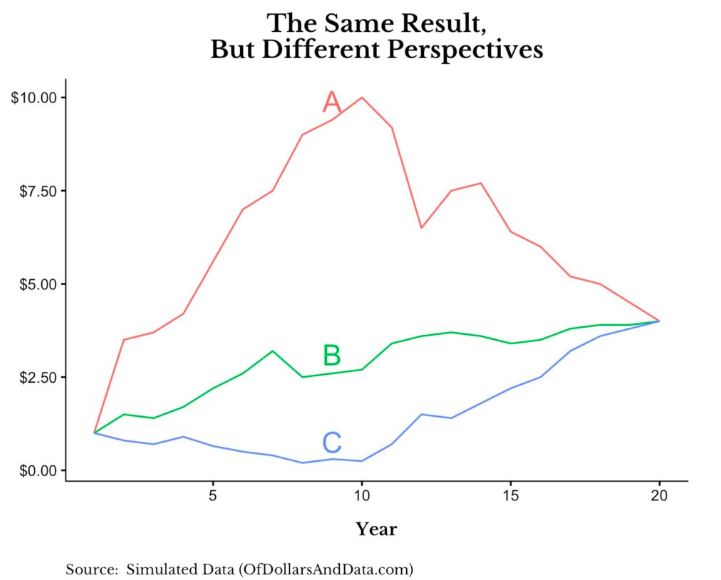

Consider the chart below. Let’s assume that each line represents the performance of a different asset class over a 20-year period. As you can see, they each end up at the same point, but over the period, asset class A is clearly a lot more volatile than asset class C.

You might say “I’ll pick asset class B – it’s a smoother ride, with less volatility.” But, we have seen instances where investors become frustrated because they hear about the strong performance of US equities and forget that they are not 100% invested in the S&P 500 Index – nor should they be!

As a student of behavioral finance, I observe human behaviors pertaining to money choices every day (including my own!)

Behavioral finance proposes psychology-based theories to explain stock market anomalies, such as severe rises or falls in stock price. The purpose is to identify and understand why people make certain financial choices. Within behavioral finance, it is assumed the information structure and the characteristics of market participants systematically influence individuals’ investment decisions as well as market outcomes. (source: Investopedia)

Given no one knows the future, the most important question to ask yourself and your investment advisor is are your investments and allocations appropriate for you?

- Understand your underlying tendencies – your behavior. Are you conservative, moderate, or a risk-taker?

- Understand how you are invested, considering first how much risk you are willing to take. You don’t need to “know it all” (that’s our job), but you do need to know whether you are comfortable with your current allocations and the amount of potential risk you are taking.

And of course, save early and often. This is often the best approach for building wealth – and one that’s controllable.

How we manage market risk.

Our clients know that we apply a data-driven approach to our investment selection process, with our models being the main drivers in our decision making process. My experience in institutional money management allowed me to understand the importance of implementing sound risk mitigation strategies, and to develop an approach that seeks to help individuals and families weather catastrophic bear markets.

The status of our proprietary portfolios is as follows:

- Our “offensive” portfolios are still largely on a buy signal, though I am holding about 10% cash to enable me to hopefully be opportunistic and buy at lower levels.

- Our “defensive” portfolios equity’ exposure ranges from 0% with our bond ladder portfolios, to a high of approximately 70% in our Risk Managed Portfolio. Our Dynamic Balanced Portfolio is currently 50% invested in equities, but the model is indicating another “sell” signal so equity exposure will be reduced further as of the beginning of November.

Our goal is to not end up at the same point regardless of the strategy, like the illustration above. Rather, our goal is to apply a combination of strategies that strive to help our clients build wealth. And we are happy to be the “tortoise” and not the “hare,” understanding that losing less may be a critical consideration for most individuals and families.

Conclusion

Year-end has historically been a positive time in the stock market, with equities rallying as money managers aim to “dress up” their performance for the year. Between now and then, however, mid-term elections loom large, with the possibility of congress being split – the House swinging back to the Democrats and the Senate remaining Republican. Regardless of one’s political views, this could be a positive for the markets, giving more balance to policies that can be detrimental to economic growth, such as tariffs.

While cyclical (shorter-term) risks have increased, we believe that the secular (longer-term) bull market remains intact – at least for now. However, no one knows what will happen next. That’s uncontrollable. However, what is controllable is having a clear understanding of your behaviors and appetite for risk, and reviewing your allocations.

Give us a call if we can help.