The phrase “sell in May and go away” is a take on an old English saying, “Sell in May and go away, and come on back on St. Leger’s Day.” This phrase refers to the custom of bankers leaving the City of London (London’s financial district) to go to the country to escape the heat during the summer months. St. Leger’s Day refers to the St. Leger’s Stakes, a thoroughbred horse race in mid-September and the last leg of the British Triple Crown, which marked the end of the summer holidays. Like all things related to the markets, there are no absolutes. However, we believe that this saying carries some weight, and may be worth considering.

This month, we review what happened in the markets during the first quarter of this year, as well as key themes that may influence market behavior over the coming months – including “sell in May.”

What happened in the First Quarter of 2017? Key Theme: Favorable

- Global Economy. The global economy continued to stabilize, with GDP growth across the major developed economies moving towards the 2% mark. Central bank policies of low interest rates (reducing the cost of borrowing), as well as adding liquidity to the banking system through Quantitative Easing (increasing lending capacity), continued to support the global economy.

- Equities. US equities continued to rally with the S&P 500 Index up 5.5%. While growing uncertainty surrounding U.S. economic policy caused a post-election reversal in policy-related sectors (e.g., financials and industrials), stock market volatility remained at extremely low levels. Given the backdrop of a weaker US dollar, non-US equities also provided a solid return with the Europe, Australasia and Far East (EAFE) Index up 4.7%.

- Bonds. Barclay’s Capital Aggregate Bond Index was up 0.8%. The specter of higher interest rates given a stronger economy and potential inflationary policies coming out of the White House (e.g., trade protectionism) pushed bond yields up and bond prices down during the course of the quarter – before reversing in March.

Key Themes for the Next Quarter: Cautious

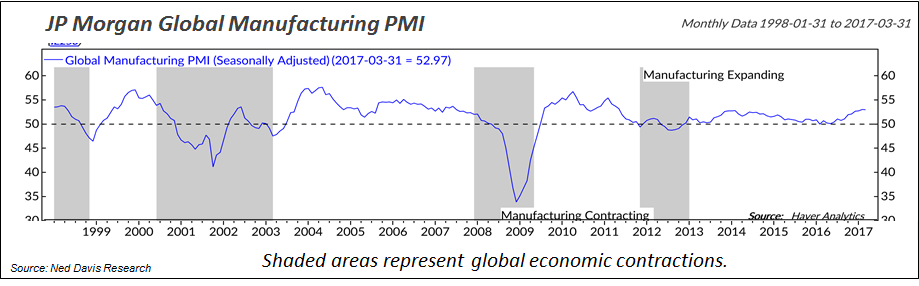

- Continued Economic Expansion. Global manufacturing continues to put in solid performance, with the Global Purchasing Managers Index at 53.0 in March, firmly above its long-term average of 51.4 and at its highest level in nearly seven years. However, this indicator of global growth is still below past peaks in activity, where the index typically has surpassed 55. Based on these historical comparisons, there’s likely still more room for upside.

- Increasing Geopolitical Uncertainty. Saber-rattling between North Korea and the U.S. over North Korea’s nuclear capabilities, as well as the U.S. missile strikes in Syria in response to the heinous chemical weapon attack by the Assad regime, have left money managers a bit skittish. Additionally, France and Germany have key presidential elections pending, and the status of Brexit (Britain’s exit from the European Union) is once again front and center.

- France’s leading contenders are both conservative. Francois Fillon is more moderate than Le Pen, and is likely to be the winner. Whatever the result, the new presidency is set to usher in a new age of right-wing politics for France after decades of centrism.

- Angela Merkel will run for a fourth term as Chancellor. Despite coming under scathing criticism for her immigration policies, Merkel is likely to win another term.

- This week, Teresa May, the British Prime Minister, called for a snap general election in June in an effort to strengthen her political backing in the negotiations for Brexit. The outcome of the election will likely impact the timing of the Brexit and create more uncertainty.

- Market Seasonality. Historically, most equity market returns are made from November through April each year. Because this phenomenon doesn’t work every year, many discount it.

However, it’s worth considering that we are about to enter the “unfavorable season” from May through October. The data proves this out. Michael Fuerst and fellow University of Miami professors wrote a paper on this phenomenon in 2012. Their report shows that on average, stock returns are about 10 percentage points higher in November-April half-year periods than in May-October half-year periods. They also found the “Sell in May” effect pervasive in other global equity markets.

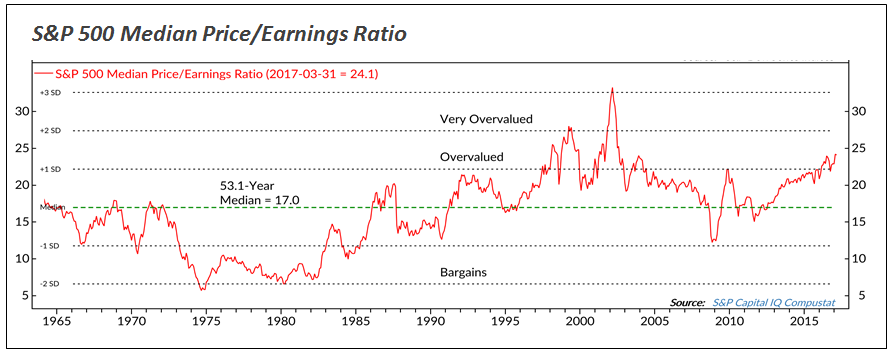

- Market Valuation. While equity markets could always theoretically go higher, US equity markets continue to be expensive by historical standards. The combination of the time of year, heightened geopolitical tensions, and valuations may leave the market vulnerable to a correction.

Key Theme for the Longer Term: Constructive

- Low Risk of Recession. The stock market historically has been a good predictor of a recession. The probability of a recession in the next 12-18 months is likely minimal. While fiscal policy remains uncertain, odds are that Trump and Congress will push through some form of fiscal stimulus that will continue to bolster growth.

- European Economic Growth on the Horizon. Faster economic growth is likely in the coming months, helped by the European Central Bank’s Quantitative Easing policies. But substantial upside potential is likely limited due to an ebbing labor force and weak productivity trends. Brexit and several major European elections, namely the French presidential election, will remain geopolitical risks in the region.

- Improved Corporate Earnings. Given the stabilization and likely economic expansion of global economies, corporate earnings are likely to continue to improve.

- Shift in Focus. The bull market that started in March 2009 has largely been driven by the Fed’s policies of lower interest rates and Quantitative Easing. The focus is now shifting to corporate earnings – that is, as the Fed raises interest rates, will corporate profits be strong enough to drive equity market returns without an accommodative interest rate environment? This is synonymous with taking the training wheels off a bike – will the child be able to keep the bike steady and perhaps even accelerate?

- Higher Interest Rates. Higher interest rates are not good for bond fund holders, that’s for certain – as interest rates go up, bond fund prices will go down. We are now in the third year of a tightening interest rate cycle, the first rate hike being in December 2015 and the second in December 2016. There has been discussion of three rate hikes this year. However, the level cannot be ignored, either. Even a fifth rate hike by the end of 2017 would keep the Federal Funds Rate below 1.5%.

Whether or not rate hikes slow the stock market in 2017 will depend on whether the Fed is forced to move faster than its current slow-paced plan. If there is an inflation shock and the Fed is forced to move fast, such a spike in rates could destabilize equity markets. However, if the pace and size of the rate increases are incremental, then there will likely be little impact on equities—at least until bond coupons seem like a better value than dividends paid on stocks.

Conclusion

Given valuations and the fact that equity markets haven’t experienced a correction since January 2016, we think that caution is warranted over the next few months. However, barring any major geo-political event and/or spike in inflation, we think that the global economy is on more solid footing than it has been for years, and will support a rising equity market, particularly as we move into year-end. As such, we will likely use any weakness over the coming months to add to our positions.

Be intentional. Be informed.

Roberta