The months between May and September have historically been when equities exhibit their greatest volatility, but this year seems to be the exception. With US equity volatility at historically low levels, a high price-to-earnings ratio and no correction of even 5% in over a year, what can we expect for the 2nd half of the year?

In short, while we may get a bit of “blowing off steam” between now and early October – which would be very healthy for the market – the wind continues to be at the back of the US equity markets. And international equities are finally showing strength after lagging US equities since 2011.

What’s driving this global equity boom?

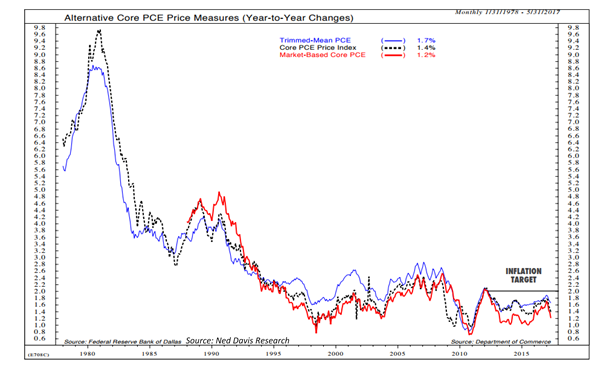

- Low Inflation And accompanying low interest rates. Central banks around the world have remained accommodative in their monetary (interest rate) policy – only the Federal Reserve has started to raise rates. However, history has shown that equities can continue to rally in spite of higher rates – as long as the rate hikes are gradual, and until higher rates begin to impact economic growth. US inflation is struggling to get back on target, reinforcing the probability that the Fed will continue its “go slow” approach to raising rates.

- No Recession in Sight With the support of central bank policies, the probability of a global recession has significantly diminished over the last year.

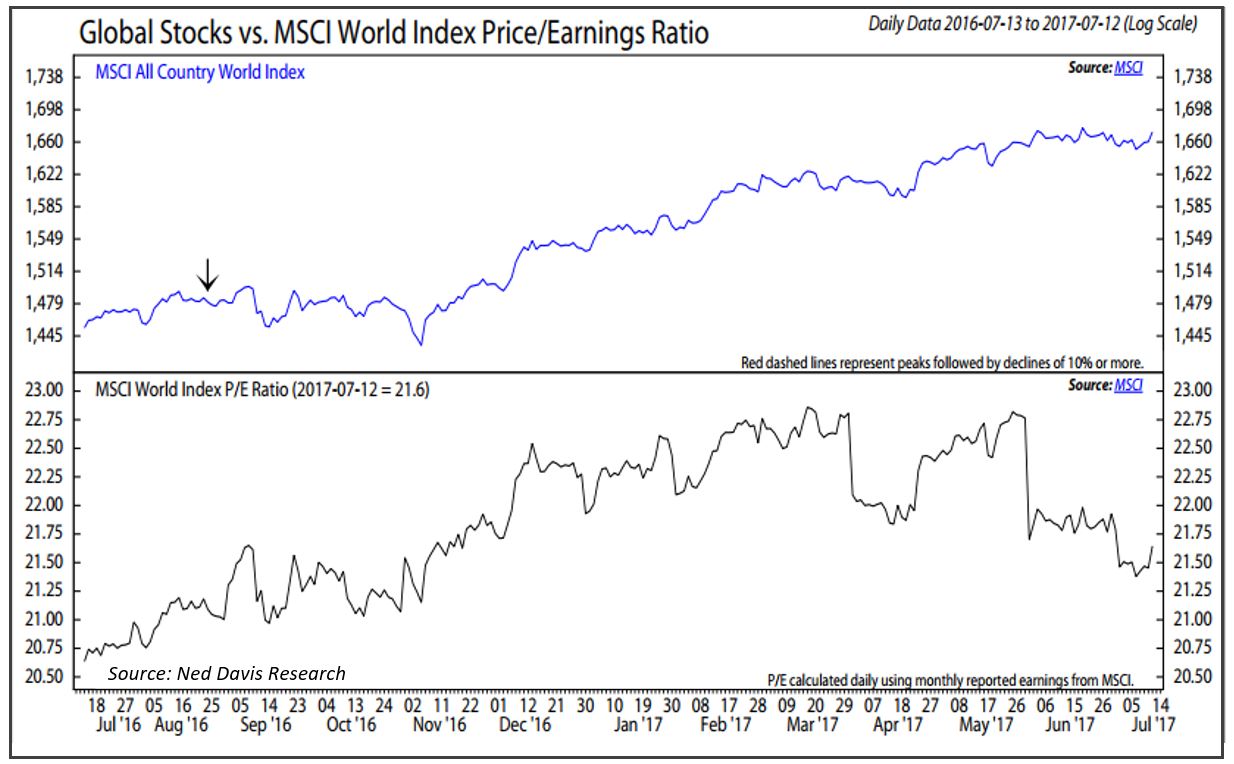

- Improved Corporate Earnings While there has been much concern regarding the high P/E ratio of US equities, it’s worth considering that there are two components to this ratio – price (P) and earnings (E). Prices of U.S. equities may be high, but over the past few quarters, earnings growth has started to serve as an offset.

On a global basis (“global” includes US and international), the earnings recovery is broadening out – with “E” rising faster than “P” for the MSCI World Index. As you can see below, this P/E ratio has reached new lows for the year, even as the MSCI World Index has remained close to record highs. And the current forward estimates for the global benchmark points to positive earnings growth for the rest of the year, which should keep P/E expansion in check.

What might cause a correction between now and early October?

- Low Complacency Volatility, as measured by the Volatility Index (VIX) is at extremely low levels. When complacency among market participants is low, the historical data show that this can actually result in increased volatility.

- Congressional Gridlock Need I say more? Trump submitted his budget in May, and in April, Congress agreed on a $1.07 trillion spending bill to fund the federal government – but only until the end of September, the remainder of this fiscal year. While we don’t doubt that a budget will be passed, it likely won’t be a smooth process, and as such, may trigger market volatility.

- Geopolitical Events Kim Jung-un, North Korea’s leader, is extremely unpredictable at best. He has repeatedly demonstrated his goal of expanding the country’s nuclear program – specifically its geographic reach – through various missile launches. It is highly unlikely that the US or its’ allies would launch a preemptive strike given the devastation that would follow. This is the difficulty that military planners face as they try to keep “all options on the table” in how to deal with this threat.

In conclusion, we expect global equities to continue their march higher into year-end – particularly after we move into the fall. We see the greatest upside opportunities in international equities, given that they have a lot of catching up to do.

As always, feel free to call if you would like to discuss this post, or if we can assist you with your planning needs.

Be informed.