The adage “sell in May and go away” doesn’t seem to be holding true this year – at least not so far. The S&P 500 is up over 16% for the year, and has now been more than 125 market days without a 5% or greater pullback. (The average since 1979 has been 51 days and the average since 2000 has been 35 days.) The length and strength of the uptrend has surprised us, as well as other money managers. We are aware that markets can get overbought/overdone to the upside (and downside) well past “market seers’” expectations. Remember the market rally of the mid-to-late 1990’s? Valuations were stretched for months, if not years. And even then, it took from late March of 2000 to early October (over 6 months) for the market to form a top and begin its descent.

The idea of not fighting the trend is currently evident in major U.S. indices, such as the S&P 500 and the DJIA. Sectors such as financials, healthcare and consumer discretionary are showing the strongest momentum in our sector model component. In late April, consumer sectors broke above their five-year uptrend, taking a decisive lead over commodity sectors, which have struggled of late (see chart below).

With central banks around the world following the lead of the U.S. Federal Reserve by lowering key interest rates, Japan and others have watched their markets soar. While European equity indices generally remain further from their all-time highs, many indices have now recouped most if not all of their losses since the sovereign debt crisis sell-off in August 2011.

Despite being extended, all of these areas continue to push “the tape” (price) to the upside. And while the upside may be limited until we see a pull back, this does not mean that global markets can’t continue to go up further – what is often referred to as a market “melt up.”

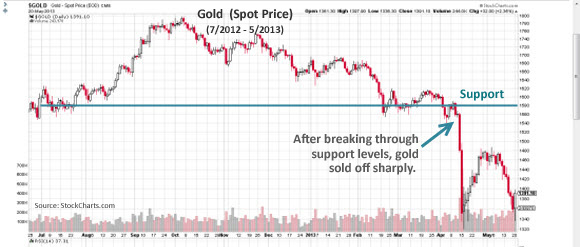

Changing expectations regarding access to credit appears to explain much of this leadership, as well as support for its continuation. This combined with the beginning of “The Great Rotation” out of bonds and into stocks (the topic of my next blog) is helping to push markets upward. And the plunge in commodity prices, gold in particular, suggests concerns over inflationary risks are, at least for now, subsiding.

We still think a moderate sell-off is likely, but any weakness will be taking place within a continuing cyclical bull market – and an improving secular bull market. As long consumers continue to spend, aided by a falling unemployment rate, and as long as the Fed remains accommodative, the economic expansion should continue, and corrections should be viewed in the context of a cyclical bull.

Alexis Advisors LLC is a registered investment advisor with the Commonwealth of Virginia. Information and concepts contained herein are for informational purposes only and should not be considered investment advice, nor is it intended as an offer or solicitation with respect to the purchase or sale of any security. Advice may only be provided after entering into an advisory agreement with the Advisor. Information is at a period in time and subject to change. Please see our Disclosures document for further disclosures and definitions contained in this article.