We apologize for the lateness of this newsletter. Laura and I have had a busy start to the year, including preparing for our new employee, Paige Harland. Paige just joined us this past week and will be a financial advisor, supporting us primarily in financial planning and marketing. Please welcome Paige!

Last year was filled with many surprising twists and turns, the most prominent being the outcome of the U.S. presidential election. Markets reflected a high degree of uncertainty for most of the year, with most money managers expecting significant volatility leading up to or after the election. Trump’s win took most of the nation by surprise; however, markets tend to digest news very rapidly – and quickly interpreted his election as a positive for the economy.

What can we expect over the coming year? We have broken down our perspective by global region and asset class.

Domestic Markets: Entangled by Politics

Trump Takes Hold of Fiscal Policy: The Upside

Obama left the White House with the economy in very good shape – with the unemployment rate at 4.7%, near a nine-year low. The Federal Reserve’s (the “Fed”) actions of raising interest rates in December reinforced this view of a firmer economy. For now, the markets have interpreted Trump’s victory as a positive, and the probability of a U.S. recession continues to be low. And Trump’s promise of lower taxes, less regulation and increased infrastructure spending are potentially supportive of higher equity prices.

Trump Takes Hold: The Downside

However, the question becomes: can Trump actually implement these policies? Republicans hold the majority in Congress, but the jury is still out regarding their level of support for his agenda. And, if his proposed policies are implemented, will they over-stimulate the economy, resulting in higher inflation, and therefore, higher interest rates?

Another consideration is the new administration’s shift towards trade protectionism. We believe this could, over time, result in significant market disruption. As of Monday, Trump signed two executive orders: 1) to renegotiate the North Atlantic Free Trade Agreement (NAFTA); and 2) the U.S.’s withdrawal from the Trans-Pacific Partnership (TPP) free trade agreement. Like “Brexit,” the British exit from the European Union (EU), which had similar drivers of trade protectionism and anti-immigration, the impact may not be felt immediately, but over time, could have a significant impact on our economy – and therefore our equity markets.

It should be noted that Trump’s policies may be market friendly, but reduced regulation comes with a potential price to the consumer of financial services and products. The Dodd-Frank Act, which was put in place after the Financial Crisis, and more recently, the Department of Labor’s Fiduciary Rule, are both intended to protect the consumer from an industry that has a “caveat emptor”– buyer beware – approach to doing business. If these regulations are reduced or rolled-back, consumers need to take note and do an extra bit of homework before working with an advisor or purchasing financial products.

Overall, a Forecast for U.S. Economic Growth

We expect continued economic growth over the course of the year, with U.S. equities ending the year up 5-8% (which, as readers know, is just a guess!). That said, we expect intermittent market volatility, particularly as we head into the second half of the year.

International Markets: A Mixed Bag

Anti-Globalization Causing Ripples in Britain & European Markets

Britain’s exit from the European Union (“Brexit”) was a trigger for central banks to unleash a new round of central bank liquidity, or at the very least, a delay in tightening. As a result, Europe is likely to continue to benefit from lower interest rates as it digests the impact of “Brexit.”

However, Britain likely has the least favorable equity outlook, given the continued uncertainty regarding the impact of “Brexit,” and Prime Minister Theresa May’s promise of a “hard Brexit” rather than a gradual disassociation with the EU. A “hard Brexit” will be felt particularly by consumers, with the price of food and consumer goods rising, resulting in a dampening of economic growth – and equity markets.

A Mixed Bag for Emerging Markets

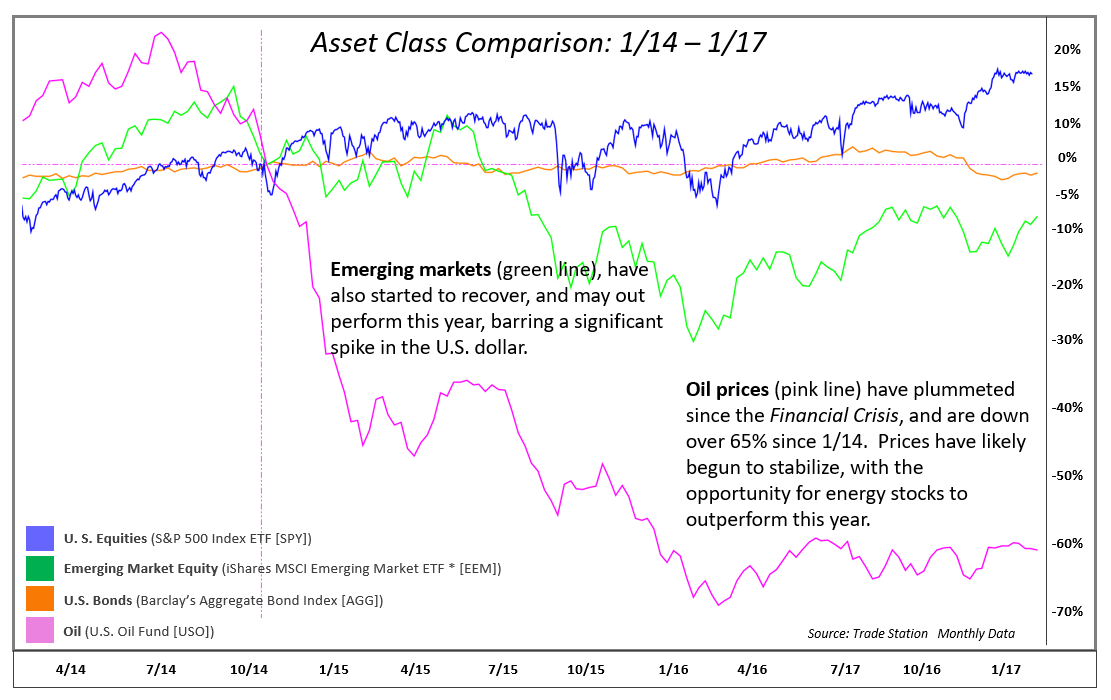

Emerging markets are likely to benefit from a broadening out of the global economic recovery – assuming that there is not a significant spike in the U.S. dollar. Emerging markets have underperformed U.S. markets considerably over the past years, providing the opportunity for outperformance in the coming period. That said, not all emerging market economies stand to benefit equally – those that are impacted by protectionist policies, such as Mexico and Canada, will likely suffer if Trump is successful in renegotiating NAFTA. On the other hand, energy-producing countries, including Russia, should benefit from the likely rise in oil.

Barring an exogenous shock, we see the end of the global recession over the coming year, which should bolster global equity markets. However, every year has its themes. Where are the likely greatest opportunities over the coming year?

Sectors & Asset Class Analysis

Yes, Different Sectors & Asset Classes Can Outperform

Money managers the world over tend to assess opportunities gained and lost over the past year, as well as the year ahead. Money managers understand that economic cycles, interest rate policies, and government policies tend to affect how asset classes and stocks in particular sectors perform. For example, most money managers understood that healthcare stocks would perform exceptionally well after the passage of the Affordable Care Act; and that declining interest rates would benefit Real Estate Investment Trusts (REITs) – but be a detriment to financial stocks.

What are the themes for the upcoming year? Which sectors and asset classes are most likely to outperform?

Energy – Are We Through the Worst?

Energy prices have been in a ditch for the past several years. Energy prices, as exhibited U.S. Oil Fund (USO), declined by over 65% from June 2014 to January 2016. That said, 2016 likely marked the bottom of energy prices, and we expect prices to continue to rally in 2017, with the energy sector likely outperforming the broader market (e.g., the S&P 500 Index.)

Alexis Advisors does not directly invest in fossil fuel companies, and will only hold small positions in energy Exchange Traded Funds – in essence, we believe that where we invest our money and our clients’ money is the equivalent of placing a vote, and we prefer not to place a vote for companies that have the potential to do great harm to the environment. (We will invest in companies that have a focus on alternative energy, however.)

Given we won’t be investing in one of the most under-valued sectors, we need to look towards other sectors that are likely to outperform. Fortunately, there are a few, and in particular, two: Financial stocks will likely continue to outperform given the probability of additional rate hikes and a stronger economy. Industrials is another sector that may outperform given Trump’s goal of increased infrastructure spending. Sectors such as Utilities, REITs and Telecom are typically negatively affected by higher interest rates. While Utilities and Telecom have been in favor over the past years, this was likely primarily driven by the “search for yield” given the very low yield on bonds. Now that interest rates, and thus yields on bonds, have begun to rise, these “bond proxies” are likely to underperform.

U.S. Bonds – Are They Safe?

This leads us to a discussion on bonds. There are many types of bonds available for purchase – Treasury bonds are issued by the U.S. government; municipal bonds are issued by specific states and/or municipalities; and corporate bonds are issued by corporations. All bonds serve as a tool to raise money for the issuer, in exchange for paying the buyer interest, which is known as the “coupon.”

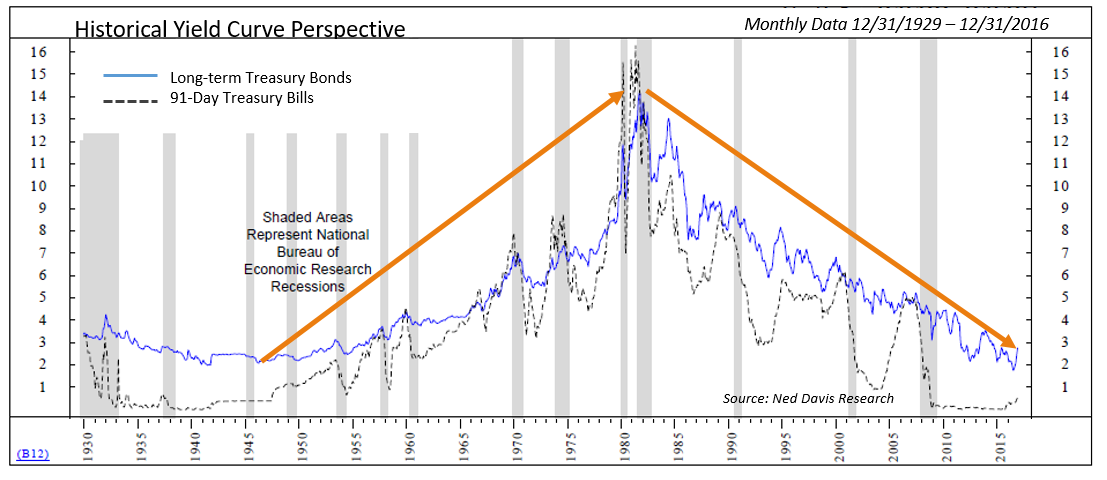

Bonds are considered “safe” investments. But as with any investment, one has to dig into the details – and with bonds, the details include the type of bond, its credit rating, whether it is a bond or a bond fund, and where we are in the interest rate cycle (see chart).

As you can see, interest rate cycles tend to be very protracted. From a historical perspective, we have had two very long interest rate cycles – one beginning in the 1940’s and ending in the early 1980’s, and another beginning in the early 1980’s and likely ending in 2015.

If interest rates bottomed in 2015, are they likely to rise for the next 20 – 30 years? Of course, we won’t know for quite some time if 2015 was the low, and will be followed by consistently increasing rates. But our guess is that this will be the case.

Rising interest rates can pose a real challenge for bond investors – particularly bond fund investors. All else being equal, when rates rise, bond prices fall (and vice versa). That means a portfolio of bonds or bond funds could see some price swings when interest rates start to move.

Bond funds hold a diversified basket of bonds with varying maturity dates and yields. However, unlike individual bonds, bond funds typically don’t have a set maturity date, because they often buy and sell bonds before they mature – and bond funds have no obligation to return your principal, initial investment. This is a very important distinction – individual bonds, unless they default, are required to return your initial investment.

If you are holding bond funds as your primary tool to offset the risk in your equity investments, we encourage you to dig a bit deeper – if you work with an advisor, speak with him/her about other tools for managing risk. We have other tools in our toolkit to help mitigate risk. While this does not mean that these “other tools” will never lose money, they at least are not guaranteed to lose money, which is the case of bond funds in a rising interest rate environment.

Wrap Up – Subscribe to Stay Informed

We expect ongoing improvement in global economic growth over the course of the year, reflecting stable-to-slightly-faster growth among both developed and emerging economies. Global monetary policy will likely remain accommodative in aggregate, resulting in moderate economic growth and higher equity prices. Although our outlook is positive, there are, as always, downside risks. For the upcoming year, these likely include an uncertain political environment in Europe, emerging market vulnerability due to a stronger dollar, and subdued trade exacerbated by protectionist policies.

Feel free to give us a call if you would like to discuss any aspects of our outlook for the upcoming year.

Otherwise, please follow us on Facebook and LinkedIn. Over the coming months, we plan to expand our presence on both sites in an effort to keep you informed on a timelier basis – about topics that directly impact your ability to meet your life and financial goals.

Be intentional. Be informed.

Roberta