Parents all know that paying for college is hard. It’s expensive, and the price tag keeps on climbing—tuition rises faster than inflation and has more than doubled in the past 30 years. It can also be confusing to navigate the sea of federal loans, institutional aid, and other funding options.

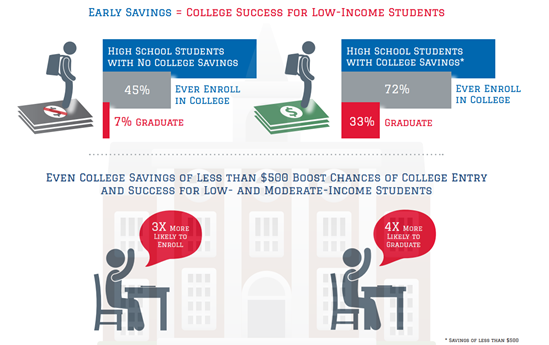

The best way to minimize this headache is to plan ahead and put money into an account earmarked for university regularly, even if all you can afford to squirrel away is pennies from beneath your couch cushions. A great bonus to saving for your child’s education is that just having that savings account makes them more likely to enroll in and graduate from college.

There are a variety of options available to help you save for college costs—prepaid plans, Coverdell savings accounts, and UGMAs, to name a few. A great place to start is with a 529 plan for the simplicity, low cost, and tax benefits. 529s offer tax-free growth and distributions (for eligible college expenses), and many states even offer a state tax deduction on contributions to the state’s plan, including Virginia.

As always, feel free to reach out if you need help sorting through your different options. But to get you started, here are some guidelines to help you make the most of 529 plans within your overall college funding strategy.

- Start early. It’s never too soon to begin saving—and saving now means borrowing less later. The earlier you begin, the more time there is for the money to grow and compound. Ideal timing would be to open a 529 account shortly after your child is born, but better late than never. Side note for those who love to plan ahead: you can open a 529 account even if you don’t have a child yet by making yourself the beneficiary and changing it to your child after they’re born.

- Set it and forget it. As with retirement savings, automating contributions is the best way to go. Calculate what dollar amount fits into your monthly budget or use this calculator to figure out how much you should contribute based on savings goal, expected growth, and forecasted tuition prices.

- Comparison shop. Each state has its own (or several) 529 plans, which vary by performance, fees, and state tax deductions. Virginia residents can breathe a sigh of relief: Virginia’s Invest529 is one of only three plans nationwide ranked Gold by Morningstar for its good performance and low fees.

- Don’t worry about the impact on financial aid. Expected Family Contribution (EFC), which is used to determine how much financial aid your child is eligible for, adds in only 5.64% of parents’ non-retirement assets, including 529s.

- Invest your savings wisely. 529s only let you change the underlying investments twice per year. When making this choice, aim for diversification and a level of risk appropriate to the amount of time left until your child starts college. An option for risk management is target date funds. While there are some drawbacks to using them, these “age-based” funds will automatically shift the allocations for you, investing more heavily in bonds or other less risky investments as college draws near. Another factor to consider is the expense ratio, which is basically the fund’s price tag—how much of your money gets deducted over the course of each year to cover administrative and management costs. The lower, the better.

- Let family pitch in. If grandparents or other relatives want to pitch in, great! If they’ll be making sizeable contributions and your college funding strategy relies on financial aid*, you may want to consider having them open their own 529 account with your child as the beneficiary. By holding off on using these funds until the second semester of sophomore year or later, these funds won’t affect your child’s financial aid eligibility. (EFC is calculated on a prior-prior-year basis—and distributions from relatives’ 529s are considered student income, which is calculated into EFC at 50%.) On the other hand, if you choose to have relatives contribute into your 529 account, that will increase the amount of state tax deduction you, as the account owner, will get next April (up to $4,000 per account in Virginia.)

- Strive for balance. Education is important and it’s great to want to help your kids pay for it, but your other financial goals are important too. Try to find the right balance between college savings and the competing demands of current income need and retirement savings. Talk to a financial planner if you need help budgeting or if you’re not sure whether you’re on track for retirement.

- Go see a free baseball game. No joke—that’s a perk of owning a Virginia 529 plan!

*If you’re not sure how much financial aid your child will be eligible for, you can get a rough idea by using the FAFSA4caster tool from the Department of Education.