Giving is a heart-centered practice. Please give to an organization that aligns with your heart. Even if it’s just a little, it can have a big impact.

Below is a list of organizations that need your support and that align with current community challenges.

- YWCA Richmond

- The Better Housing Coalition

- Partnership for the Future

- Sister Fund

- Urban League of Greater Richmond

- Peter Paul Development Center

- The Innerwork Center

WE ARE ALL IN THIS TOGETHER – NOW IS THE TIME TO GIVE

Non-profits and around the country are feeling the pinch of a slowing economy. Now is the time to give, even if it’s just a little.

The Federal Government has passed legislation to encourage giving by offering more tax incentives. There is a strategy for smart gifting for every tax situation.

It’s tough to keep the laws straight – The Tax Cut & Jobs Act, The SECURE Act, and the recently passed CARES Act. We are not going to worry about the names, but rather going to boil down the opportunity by tax category. This will allow you quickly see which giving options best suit you and your circumstances.

Please note that some of the strategies outlined below are not new, but we have included them as they are equally valuable to the charity as the options recently made available.

CHARITABLE CONTRIBUTIONS: AVAILABLE TO NON-ITEMIZERS

Itemized deductions are expenses allowed by the IRS to decrease your taxable income. There are dozens of itemized deductions available. These expenses can exceed the standard deduction, meaning that itemizing on your tax return can make a huge difference in your tax bill.

With the tax law changes of 2018, standard deductions were increased considerably, resulting in over 90% of us no longer able to take advantage of itemizing. And you can take either the standard deduction or itemized deductions – you can’t do both.

One of the recent initiatives passed by the government to bolster non-profits to offer those who don’t itemize is a tax deduction of up to $300 per taxpayer ($600 for a married couple). Contributions must be made directly to a charity, and not to a Donor Advised Fund. Essentially, these donations will reduce your adjusted gross income (AGI), and thereby reduce taxable income.

GIFTING STOCK

All charities appreciate the gift of cash. But another strategy that is available to anyone who owns stock in a publicly traded company is to gift the stock.

I was fortunate enough to inherit stock from my parents. There was one stock in particular that represented too much of my account. It had been purchased decades ago and as result, had appreciated significantly. It was also held in a brokerage (taxable) account, so to sell it would have resulted in a sizable capital gain. Rather than sell, I decided to gift a portion of the stock to two qualified non-profits – one near and dear to my family (Sheltering Arms Rehabilitation Center), and the other near and dear to me (The Innerwork Center.)

You may be in a similar situation, or you may be fortunate enough to have individual stock, mutual funds, exchange traded funds in a brokerage account that have appreciated significantly since you purchased it.

If you are charitably inclined, it’s more beneficial to you and the charity to gift the stock, rather than sell the stock and gift the cash. If you sell the stock, you will pay 15-20% in taxes on the gains, and, depending on your circumstances, you may also be thrown into a higher tax bracket. On the other hand, if you gift the stock you have a double benefit – you are actually giving 15-20% percent more than if you had sold the stock and paid the taxes, and you have avoided the potential headache of being bumped up to a higher tax bracket and paying more taxes!

* Corporations may deduct up to 25% of taxable income, up from the previous limit of 10%.

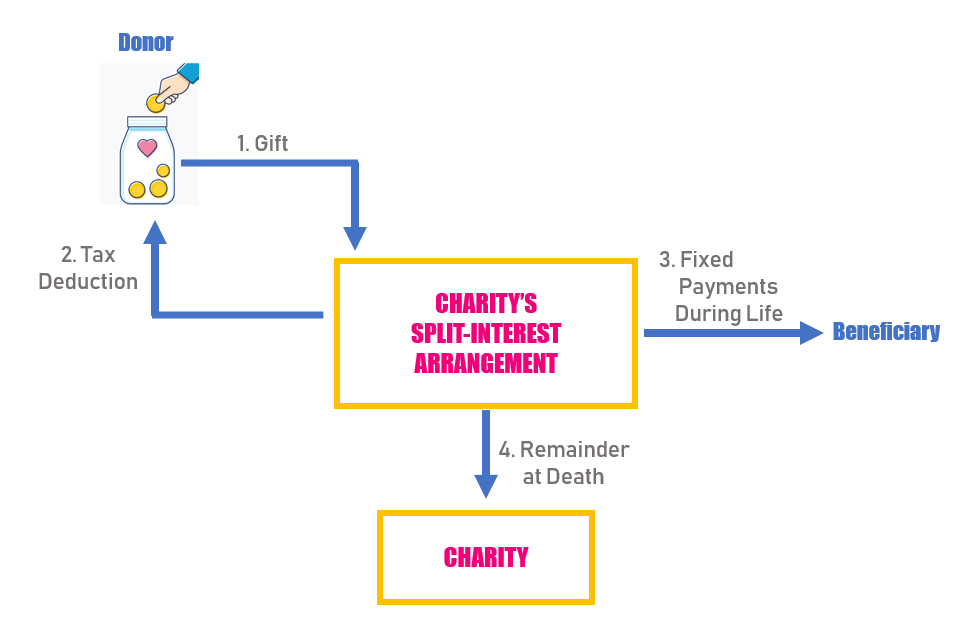

SPLIT INTEREST GIFTS: GIFTING + PENSION-LIKE INCOME

Another strategy falls under the category of split-interest gifts – this one is my favorite because it offers so many benefits to all parties. A split interest gift strategy is suitable for those who are charitably inclined, but also want or need to receive an income stream during their lifetime.

A split-interest gift is what it sounds like – the donor’s gift is split in two: an irrevocable gift made to a qualified charity; and a lifetime income stream to the donor, and at death, the residual being retained by the charity*.

There are types of split-interest arrangements. In most instances, in addition to the guaranteed income stream, donors may qualify for an immediate partial tax deduction. And with some arrangements, depending on how you fund the gift (cash or securities), a portion of the income payments may be tax-free.

Large, well established charities and educational organizations offer the administrative support for such gifts: drafting the trust, filing an annual tax return/report and preparing tax forms for the donor. They make it easy for the donor. Smart, huh? But an attorney and CPA can take care of these things for smaller charities that don’t have those same resources.

CHARITABLE CONTRIBUTIONS: AVAILABLE TO NON-ITEMIZERS

Itemized deductions are expenses allowed by the IRS to decrease your taxable income. There are dozens of itemized deductions available. These expenses can exceed the standard deduction, meaning that itemizing on your tax return can make a huge difference in your tax bill.

With the tax law changes of 2018, standard deductions were increased considerably, resulting in over 90% of us no longer able to take advantage of itemizing. And you can take either the standard deduction or itemized deductions – you can’t do both.

One of the recent initiatives passed by the government to bolster non-profits to offer those who don’t itemize is a tax deduction of up to $300 per taxpayer ($600 for a married couple). Contributions must be made directly to a charity, and not to a Donor Advised Fund. Essentially, these donations will reduce your adjusted gross income (AGI), and thereby reduce taxable income.

ITEMIZED DEDUCTIONS

For the 8% or so of individuals and families that do itemize, you can now deduct much more of your charitable contribution. In 2020, individuals can deduct cash contributions made to public charities, up to 100% of AGI. This is up from the previous limit of 60%. For example, if your AGI is $80,000, you can now make a cash contribution up to $80,000, with 100% of the $80,000 as a tax deduction.

QUALIFIED CHARITABLE DEDUCTIONS: FOR THOSE WHO TURNED 70 ½ IN 2019

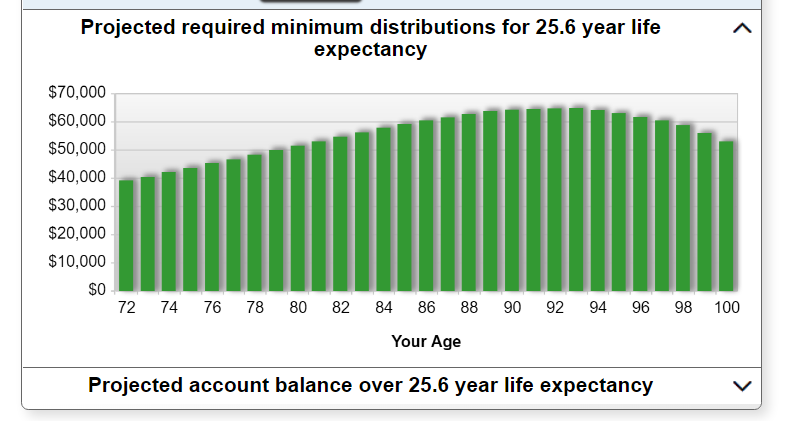

A Required Minimum Distribution (RMD) is the amount of money that must be withdrawn from a qualified retirement plan (e.g., a traditional IRA, SEP, etc.) by the owner once the owner reaches a specific age. When you take your RMD, you have to pay income taxes on the amount of the distribution, and the percentage distributed increases every year. You have no choice in the matter.

As the percentage RMD grows, your tax liability grows. Additionally, RMDs are counted as income, so if you have a large qualified plan, then these RMDs can throw you into a higher tax bracket, resulting in paying even more taxes.

For example, let’s say you have an IRA with an account balance of $1,000,000 at the end of last year. Making a number of assumptions about rates of return, age, and beneficiaries, you could end up owing $30-$60,000+ per year in RMDs! The chart below illustrates this. (Source: AARP)

I am sure you can see how a $50,000 RMD could easily throw you into a higher tax bracket.

But gifting all or a portion your RMD to a qualified charity is a great strategy that that allows you to give while also reducing your tax liability.

These types of RMD distributions to a qualified non-profit are called Qualified Charitable Distribution (QCDs). The amount gifted is not taken as a deduction, but reduces your taxable income. The maximum annual amount that can qualify for a QCD is $100,000. This applies to the sum of QCDs made to one or more qualified charities in a calendar year. However, you file taxes jointly, your spouse can also make a QCD from his or her own IRA within the same tax year for up to $100,000.

While the new CARES Act waived the RMD requirement for 2020, this does not mean you cannot take it. And while the SECURE Act increased the age to 72 for those who haven’t started their RMDs, the Act left unchanged the age at which you can make qualified charitable distributions at 70 ½.

Why would you take your RMD if you don’t have to? Three reasons:

1) Non-profits need our help.

2) This allows you to direct these funds in a tax efficient manner, and reduce your tax liability.

3) This allows you to reduce your IRA balance, and therefore reduce the amount of taxes paid over the life of your IRA – and the taxes paid by the beneficiaries of your IRA after you die.

One thing to note: To receive the tax benefits, you must give contributions directly to a qualified public charity – the same rules and exclusions prior to this new legislation apply to gifts to private foundations and Donor Advised Fund.

CONCLUSION

We have covered a lot of territory in this blog post. Please give us a call if we can help clarify any of these strategies. We work with lawyers and CPAs who are familiar with these strategies and can assist in their implementation.

Whether you can give $5, $50, $500, 5,000 or more, now is the time to help. Give what you can – and I can almost guarantee you will feel great for doing so.

In closing, a special thanks to Maureen McKay, CPA/CFP who assisted in writing and editing this blog. Maureen has been a tremendous resource to our business and to our clients.

Alexis Advisors, LLC is a registered investment advisor with the Commonwealth of Virginia. Information contained herein is for educational purposes only. Nothing in this post should be construed as advice. Advice can only be rendered after entering an advisory agreement.

Consult with an estate planning lawyer, financial planner and tax advisor when considering gifting strategies.

* All stock art is sourced through the public domain and is not copyright protected.

* In a Charitable Lead Trust arrangement, the reverse is true – during the lifetime of the donor, the charity receives a stream of payments (annuity) and at death of the donor, the remainder goes to whomever is the designated beneficiary.