What the heck are tariffs? And how do they impact your wallet?

A tariff is essentially a tax on goods as they cross national borders – a tax on imported goods entering the country. When an importer brings goods into the United States, it pays a tariff to the U.S. government—typically 10% or 20% of the price paid. Tariffs are paid by companies that import the products, not by the countries themselves. Because most businesses cannot afford to absorb these costs without significantly impacting their profitability, they typically pass them on to consumers through price increases.

Tariffs are not new. They have been used in the U.S. since 1789, initially helping to fund the new government.

Tariffs serve two main purposes: protection and revenue.

Protection

A protective tariff increases the price of imported goods compared to domestic products, encouraging consumers to buy local and shielding domestic businesses from foreign competition.

For example, when a tariff is placed on imported vehicles, the price of these vehicles increases, and domestically manufactured vehicles are relatively attractive. The intent is to make U.S. vehicles cheaper and to protect the U.S. auto industry. While this seems beneficial, there are unintended consequences: lack of competition results in higher demand, which drives prices higher. And then there is the risk that the countries supplying the parts to manufacture our cars slap on retaliatory tariffs – driving costs up further.

Another example is coffee. Some countries are better equipped to produce coffee, leaving U.S. consumers reliant upon coffee imports. When tariffs are imposed on imported coffee, producers pass the added expense on to the consumer. In this case the tariff has served to just make the cost of coffee more expensive for all of us, and the country that produces coffee beans is unaffected.

These examples illustrate that everyone – individuals and businesses – is paying more. And higher prices are the definition of inflation.

Revenue

Tariffs also generate government income. This sounds like a benefit, but most economists consider them an inefficient way for governments to raise money and promote prosperity. How do we know this? If tariffs were effective, wealthier countries would be using them as a key tool. While tariffs once made up a large portion of government revenue – over 41% in 1900—this dropped to just 2% by 2013 in wealthier countries.

The Cost of Tariffs

Experience shows and economists agree that tariffs lead to persistently higher prices for customers. In 2018 the U.S. raised import tariffs from 2.6% to 17% on over 12,000 products. This nearly always meant that the U.S customers paid higher prices for the for the affected imported goods—in fact, prices were often higher by the full amount of the tariff.

Countries that face U.S. tariffs on their imports may retaliate with their own tariffs – driving prices up further. A recent report from the Peterson Institute for International Economics said that this could result in slashing more than 1% off the U.S. economy by 2026 and make inflation 2% higher next year than it otherwise would have been.

The Potential to Go Backwards

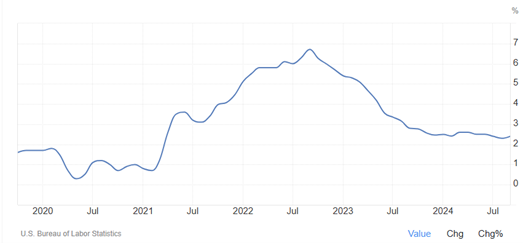

Inflation in the U.S peaked in the second half of 2022 (see chart below), reaching its highest rate since 1981.

Thanks to the Federal Reserve’s interest rate policies, the inflation rate has declined sharply, with the Consumer Price Index Core rate at 2.40% as of September.

More inflation is not what we need – particularly right now, with interest rates finally on the decline.

To combat inflation, the Federal Reserve would need to raise interest rates…again. Want to buy a home? If the Fed raises rates, mortgage rates would follow, making home ownership less attainable. Additionally, higher interest rates would add to America’s debt burden. Higher rates mean higher interest payments on the debt, just compounding the debt problem.

The ideas presented here aren’t original or unique. For a more in-depth analysis, read the article Tariffs Are Great – If You Like Raising Prices, Undermining Jobs, and Inhibiting Innovation by Matthew Rooney, Managing Director of the George W. Bush Institute.

About the Author

Roberta Keller

Roberta is passionate about the intersection of money and social impact. Her goal has been to build a business that integrates her institutional money management experience with her yoga and meditation practices.