DO YOU THINK MEDICARE IS EASY TO UNDERSTAND? THINK AGAIN.

-Kendalle Stock, Commonwealth Medicare Advisors

I have been working in the insurance business since 1985, assisting clients with many types of insurance and now solely focusing on supporting clients navigate the “Medicare maze.” Following are a few of the things that trip people up the most – things that can end up costing you money and/or impacting your benefit.

1. Medicare, HSAs, and Your Employer Plan – It’s tricky! Are you making contributions to a Health Savings Account (HSA) and plan to continue to do so? If you are working past age 65 and staying on a group health plan, (perhaps waiting for a spouse to become Medicare age), do NOT sign up for either Part A or Part B. Many people will sign up for Part A only because there is no premium involved. This poses a problem because the tax-qualified status of HSA contributions is predicated on the premise that there is NO other insurance other than your High Deductible Health Plan. Part A of Medicare IS considered “other health insurance”, which would cause loss of that tax-qualified status. Many people have gotten tripped up over this.

2. HSAs & Medicare – Lookout for “Lookback!” Another HSA “lookout” – you CAN continue to contribute to your HSA past the age of 65, but be aware that the IRS will do a six-month “look-back,” and any funds contributed for the six months prior to signing up for Medicare will lose that tax-qualified status. And the “lookback” is done on a pro-rated basis, so contributing the max amount in one lump sum before the six-month period will not have the intended outcome. It was a good thought, but the IRS is one step ahead of us.

3. Can I Use My HSA to Pay Medicare Costs? Funds in an HSA can be used to pay Part B premiums, Part D premiums, deductibles, copays, and co-insurance, if applicable. Those funds cannot be used to pay a Medicare Supplement premium, as the government does not consider that premium to be a qualified medical expense. (Not a fan of that provision, but they never asked me.) The funds can still be used to pay for things like dental and vision expenses. They do not have to be depleted in any particular time frame. It’s not a “use it or lose it” scenario.

Source: https://www.virginiapremier.com/wp-content/uploads/MedicareFactsMadeSimple.pdf

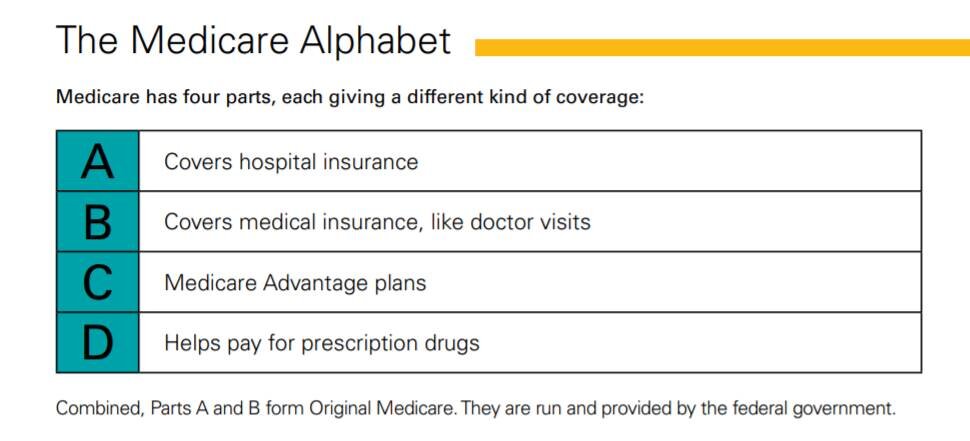

4. Should I Sign Up for Part A and B? If your group has under 20 people, then you absolutely should sign up for Medicare Part A and Part B. Under the “Who pays first?” rules, Medicare is secondary for small groups, and the group coverage will pay out accordingly. Since Medicare pays 80 percent of medical bills, your group will only pay 20 percent (after your deductible and coinsurance)— while assuming you are on Medicare. Twenty percent of, say, open heart surgery, can end up being a lot less than you would need to pay the hospital bills. Group size matters. If your group has over 20 people enrolled, then your group insurance becomes primary (they pay first), then Medicare would pay secondary. Often it comes down to “crunching the numbers” – comparing what you are paying for group coverage (factoring in deductibles and coinsurance) to what your Medicare costs would be.

5. Can Retiring Reduce Your Medicare Bill? Part B premiums are “means-tested”, which I personally think is “mean.” It is based on your income from two years ago, so this year, they would be looking at 2019 tax returns, specifically your Modified Adjusted Gross Income. If you are married and filing jointly and your MAGI two years ago was over $176,000 ($88,000 single), congratulations! You’ve done well. But your Part B premiums be surcharged (IRMAA charges). HOWEVER, if you are retiring and your income is going to drop, there’s a form for that. SSA-44. Download it here and print it. This is the way you tell the government, “Hey, I’m not making the money now that I did two years ago – here’s my projected income going forward. Calculate my Part B premium on this figure.” Try to give an accurate amount, because they WILL go behind and check. There is also a smaller IRMAA surcharge for Part D. All these amounts can be found on the SSA-44 form.

About Kendalle Stock

In 2013, Kendalle decided to focus solely on Medicare planning. Being appointed with several major Medicare carriers allows her to find the right plan for her clients’ needs and budgets. Her priority remains to make certain that her clients fully understand Medicare and all the available options. She will also help with enrollment procedures, and timelines. Timing is critical when it comes to enrolling. Need help? Kendalle will help you get it right.