If you think the stock market is complex, wait until you learn about the bond market.

I worked on a bond trading desk on Wall Street and in London for quite a few years. It was fascinating – but in the beginning, extremely overwhelming. Up until that time, I had no understanding of the complexities of the bond market.

We want readers to understand a few things about bonds, especially in today’s interest rate environment. Interest rates have started to creep up, which can have a negative impact on bond prices – particularly bond fund prices.

WHAT IS A BOND?

A bond is a type of security that represents a loan made by a lender/investor (you) to a borrower (typically corporations, mortgage companies, and government entities/agencies.) Think of it as an I.O.U. between you (the lender) and the borrower. When you buy a bond, you are essentially lending the corporation or government entity your money, and in return, they pay you interest.

Bonds are used by companies, municipalities, states, and sovereign governments to finance projects and operations. Companies can also issue stock to finance projects – but a stock technically carries more risk (and reward) than a bond – for both the investor and the lender.

HOW BIG IS THE BOND MARKET?

Big. While the stock market gets more press, the U.S. stock market total capitalization is actually a bit smaller than the bond market.

The total amount of debt owed through bonds as of March 2019 was more than $40 trillion. This figure includes more than $14.4 trillion in United States Treasury debt, more than $9.2 trillion in mortgage-related bonds, more than $8.8 trillion in corporate bonds, and more than $3.8 billion in municipal bonds.*

The stock market, on the other hand, was just over $30 trillion in total market capitalization, meaning the value of all outstanding shares.*

CAN THE BOND PRICE INCREASE AND DECREASE?

Yes. The price of both the stock and bond markets can increase and decrease based on, among many other things, supply and demand and, importantly, the Federal Reserve’s interest rate policy. It’s ever-changing.

Think about it this way – you know that a stock price can go up and down based on all sorts of factors – some related to the performance of the company, some not necessarily related. For example, during the Financial Crisis of 2007-2009, solid stocks like Apple and Microsoft got sold along with stocks of less financially stable companies.

Bonds are similar. From the time a bond is issued, the bond price can go up and down, driven by a whole host of factors – some related to the issuing entity, and some not.

SO, DOES THAT MEAN YOU CAN LOSE MONEY INVESTING IN BONDS?

It depends.

If you invest in an individual bond – say you buy one Apple bond for $1,000 – if you hold the bond until it matures, you will get your investment bank (assuming Apple doesn’t default.)

This is not how bond funds work. And this is the key point for bond fund investors to understand.

With bond mutual funds or Exchange Traded Funds (ETFs), the investor will indirectly receive interest paid by the underlying bonds held in the mutual fund. However, mutual funds are priced differently than individual bonds and the price of the fund share is based on the net asset value (NAV) of all of the underlying holdings in the fund. So, if bond prices are falling, the bond fund investor can see declines in their principal investment (the NAV of the fund can fall).

IS THIS TRUE OF ALL BOND FUNDS?

Some bond funds are riskier – more prone to losses – than others. This is where it’s important to understand what types of bond funds you are invested in.

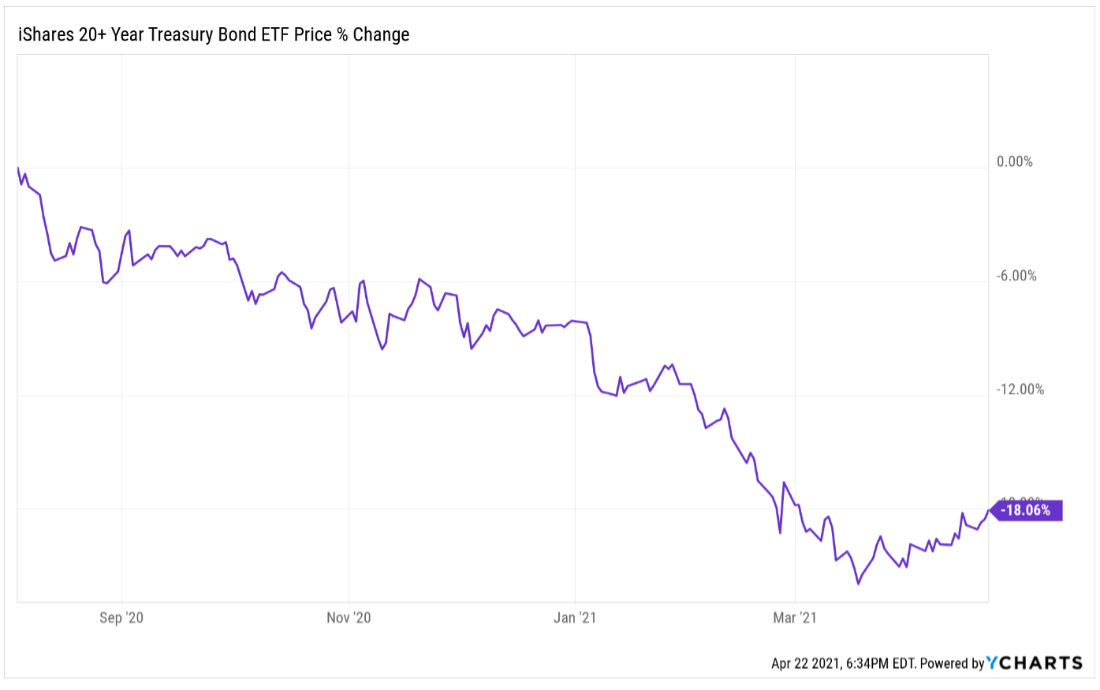

The chart below illustrates the price performance of the iShares 20+ Year Treasury Bond ETF. Most people think of Treasury bonds as extremely safe. They are if you buy an individual Treasury bond – after all, the U.S. Government is not likely to default on its obligations.

But a bond fund is a different story. As you can see, between August 4, 2020, and April 25, 2021, this bond fund lost just over 18% of its value.

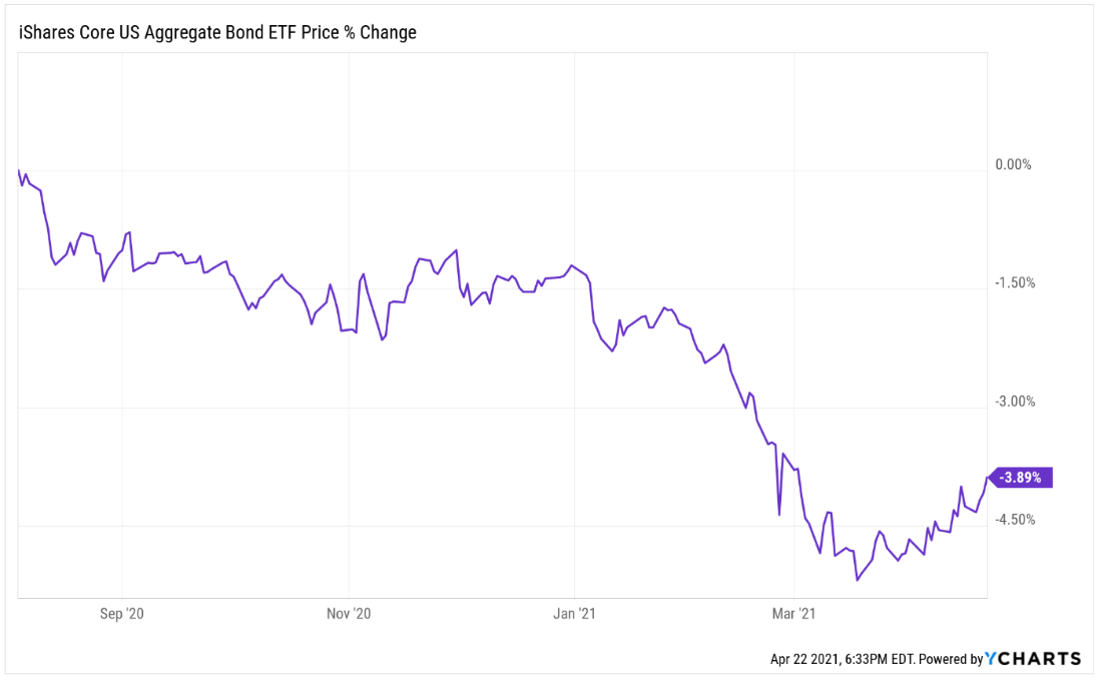

Most financial advisors don’t invest their clients in a 20+ year bond ETF, understanding the risks. A more typical bond investment is represented by the iShares Core US Aggregate Bond ETF. This fund includes a little bit of everything – government Treasury securities, corporate bonds, mortgage-backed securities (MBS), asset-backed securities (ABS), and municipal bonds to simulate the universe of bonds in the overall market. As you can see, the price decline over the same period is much less – just under 4%.

Not so bad. And at its worst point in March, it was down just under 5%.

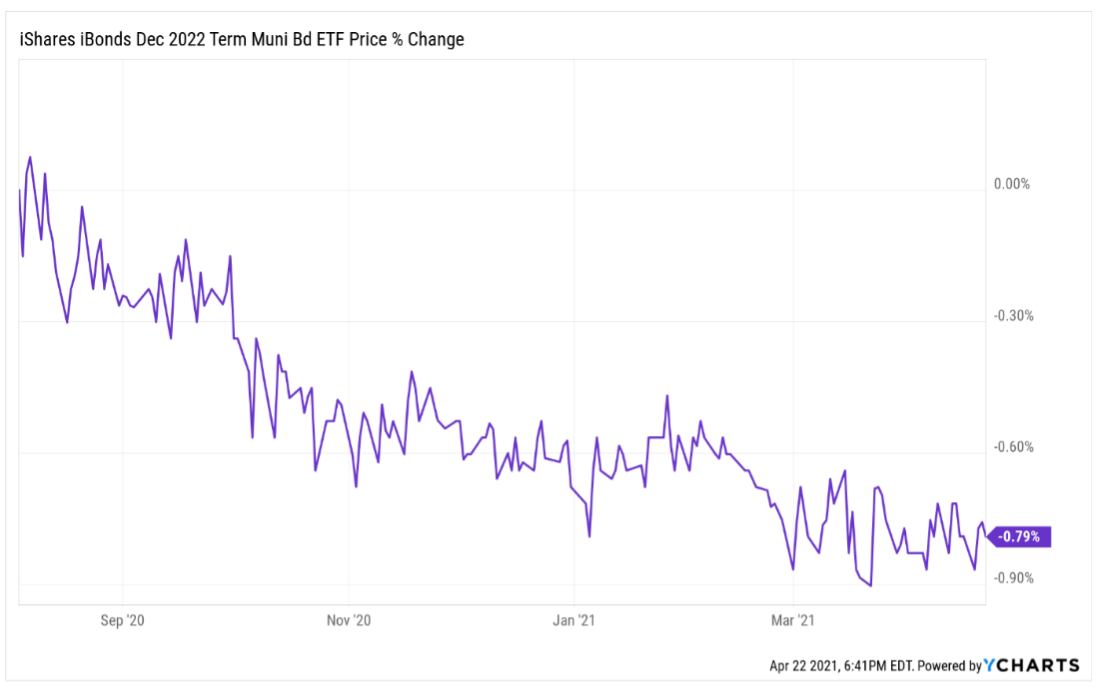

Let’s look at one more. The iShares iBond December 2022 Term Municipal Bond Fund ETF lost just under 1% over the same time period. Clearly, this is the least risky of the three.

WON’T BOND FUND PRICES GO BACK UP?

The “won’t bond mutual fund prices go back up” is tough to answer because no one knows the future. Over the past few weeks, bonds have rallied a bit. But we just don’t know if this will persist.

What we do know is that we have been in a 40-year bond bull market, where interest rates have continued to trend lower and lower, pushing bond prices up higher and higher. So while we have had a reprieve over the past few weeks, many are questioning whether we are at a key inflection point with the possibility of entering a bond bear market.

WHY WOULD THIS HAPPEN?

As mentioned above, there are a lot of drivers to bond prices – but a key one is interest rates.

A substantial number of bond fund managers are concerned about the amount of money that has been issued help weather the pandemic, and that this may lead to higher inflation. Inflation is a key factor affecting interest rates. When a surge in inflation occurs, a corresponding increase in interest rates takes place. And when interest rates go up, most bond fund prices go down.

DOES THIS MATTER?

Yes. As you can see in the charts above, it matters in what type of bond funds you are invested. What if 40% of your account is invested in a bond fund that is currently down -3.89% since last August? You may be OK with this, but what if this doubles to 8%?

WHAT SHOULD YOU DO?

The answer is not to say “I just won’t invest in bonds.” An allocation to bonds is still a very useful and important risk management tool.

But I do suggest you talk to your advisor. Ask her (or him) what she is doing to manage your bond allocation given the potential risk.

Over the past year, we have managed this “interest rate risk” by adjusting the types of bond ETFs we are investing in our portfolios. If you want to learn more, reach out. I don’t work on a bond desk anymore, but I still love talking about them! And if you want to take a deeper dive on some “fun facts” about bonds and our national debt, click here.

*Source: Zacks.com – Bond Market Size versus Stock Market Size – By: Steven Melendez – March 20190 Likes