Market seasonality refers to particular time frames when stocks/sectors/indices/commodities are influenced by recurring themes that produce patterns. Themes and the underlying “triggers” for market seasonality can range from weather events to calendar events (quarterly reporting expectations, announcements, etc.). These periods can be days of the week, months of the year, six-month stretches, or even multi-year timeframes.

The key point is that these themes are often recurring. But can they help with wealth building?

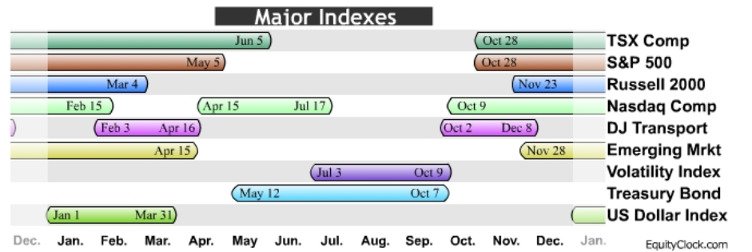

SEASONALITY & THE MAJOR INDICES

This time of year (from May through October) is often referred to as “the unfavorable season”. The Wall Street adage “sell in May and go away” refers to this period during the year, when the market on average, underperforms the prior six months of the year (November through April).

The chart below (source: EquityClock.com) shows the best performing periods of the year (colored bars) for the major indices. Unfortunately, EquityClock.com does not provide the supporting data. However, I have tracked seasonality for years and can confirm this theme but understand that this does not repeat every year.

What is most interesting about this chart is that it clearly illustrates that from October/November through April/May equity indices tend to exhibit their best performance. On the other hand, from May through October, the Volatility Index (purple bar) and Treasury Bonds (teal blue bar) exhibit their best performance. Treasury Bonds are often bought by money managers as a “safe haven” investment when equity prices are going down. Buying in any asset class – be it a Volatility Index or Treasury Bonds results in rising prices.

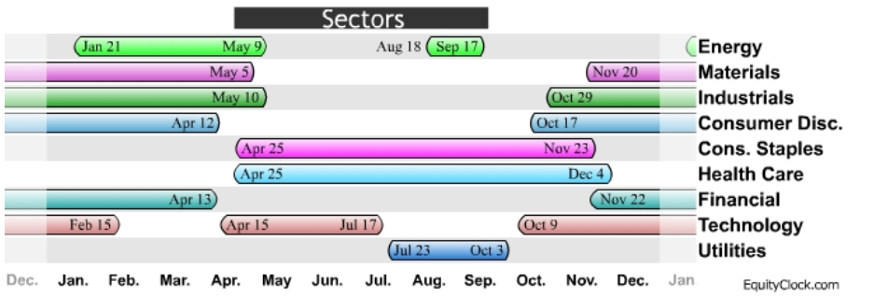

DIGGING DEEPER – SECTOR SEASONALITY

Are cycles and seasonality inside of an asset class – for example equities? The answer is “yes.”

Let’s start by defining exactly what is meant by a “sector.” A sector is an area of the economy in which businesses share the same or related business activity, product, or service. Sectors represent a large grouping of companies with similar business activities, such as technology or healthcare. Investors use sectors to group stocks and other investments into categories that share unique characteristics.

The Global Industry Classification Standard (GICS) is the primary financial industry standard for defining sector classifications. There are 11 broad sectors commonly used to classify stocks:

- Energy

- Materials

- Industrials

- Consumer Discretionary

- Consumer Staples

- Health Care

- Financials

- Information Technology

- Telecommunication Services

- Utilities

- Real Estate

Investment sectors can provide insight as to how an economy is performing and which areas of the economy are performing better than others. For example, when an economy is expanding, then Industrials, Consumer Discretionary, and Information Technology companies tend to do well as people are spending money.

When an economy is contracting (heading into or in a recession), stocks such as Health Care, Consumer Staples, and Utilities tend to perform better.

Based on this, which sectors do you think might perform better when we are in the “unfavorable” period of the year? The EquityClock.com data illustrates this well, with the three defensive sectors tending to perform better during this period. (Note: Not all GICS sectors are illustrated below.)

WHAT DOES THIS MEAN FOR 2021?

No cycle or theme is perfect, and none occurs every year.

But we are expecting a pullback or correction in equities as we head deeper into the “unfavorable” months of August, September, and October.

We haven’t had a correction (defined as a decline of -10% to -20% from an index’ recent peak) since the bear market (defined as a decline of -20% or more) in spring 2020, when the S&P 500 Index lost just over -34% from February 19th to March 23rd.

Additionally, most years, equity indices experience a -5% decline two-to-three times per year, on average.* We have not had even one in the past year!

HOW WE APPLY THESE THEMES IN OUR WEALTH MANAGEMENT APPROACH

Given the market seasonality coupled with the lack of a –5% decline over the past year, we have become slightly more defensive in our equity portfolios, buying Health Care and other defensive ETFs. The goal is to provide a bit of a buffer should we get a correction. We have also positioned our bond portfolios to capture a portion of what may continue to be an upward move in Treasury Bonds.

Wealth management and investing in the markets is a tough business. It’s humbling. It’s challenging. And it’s also incredibly interesting.

Reach out to learn more. We welcome conversation and questions!

*Source: Interactive Advisors: https://investing.interactiveadvisors.com/2014/08/often-investors-expect-5-market-corrections