A black swan year for the markets and the world! If 2020 taught us anything, it is to expect the unexpected. Proper emergency funds and risk management held some afloat during a tumultuous year.

As we put behind us one of the weirdest and most harrowing years in recent history, no one on Wall Street can say with any authority what’s next. The prediction game isn’t a good one to play, even in normal times. And we’re exiting a year when the market whipsawed from three-year lows to all-time highs amid coronavirus, the election of a new president, zero interest rates, and worldwide recessions.

With that said, we have six themes we are focusing on for the upcoming year:

- Vaccines & re-opening – Vaccines are being deployed and there is light at the end of the tunnel

- New President – We have a new president who will likely be more economically constructive than many fear

- More stimulus – We have a friendly Federal Reserve, and another stimulus package has been passed by Congress

- Search for yield – Bond yields continue near historic lows, with many searching for yield in stocks

- ESG investing – President Biden has a sharp eye on climate change, which should expand the focus on ESG investing even more

- Emerging markets – There are potentially more profitable investments outside of the United States

1. Vaccines & Re-opening

The vaccine situation is obviously still unclear, making it tough for economists to pin down the outlook with any real authority. That’s a heavy lift even in a normal year, which might remind some people of the old joke about economists predicting 10 of the last six recessions. So, while the public health threat is still present, we believe the world’s economy will likely continue to advance, albeit at a modest rate, but accelerating as the vaccine roll-out gets traction.

One of the main themes that dominated Wall Street in 2020 was the battle between “stay at home” versus “going out” stocks. Stocks like DocuSign, Netflix, Zoom, and other cloud computing stocks soared, while travel, restaurant, and hotel stocks got slammed. Financials and energy stocks also took it on the chin as a depressed world economy reduced demand for their services and banks had to build huge reserves against possible defaulting loans.

We expect significant upside opportunity in the most beaten-down stocks and sectors as the economy re-opens. And as this occurs, we don’t necessarily see an about-face in technology and other sectors that have benefited from the lockdown. Many analysts and executives are talking about the benefits of a work from home workforce.

Basically, the pandemic accelerated a lot of technologies that may have been a few years away but now are likely here to stay.

2. New President & The Blue Wave

One thing many had feared was a so-called “Blue Wave” that had a chance to bring heavier regulation on corporations and higher taxes on investments.

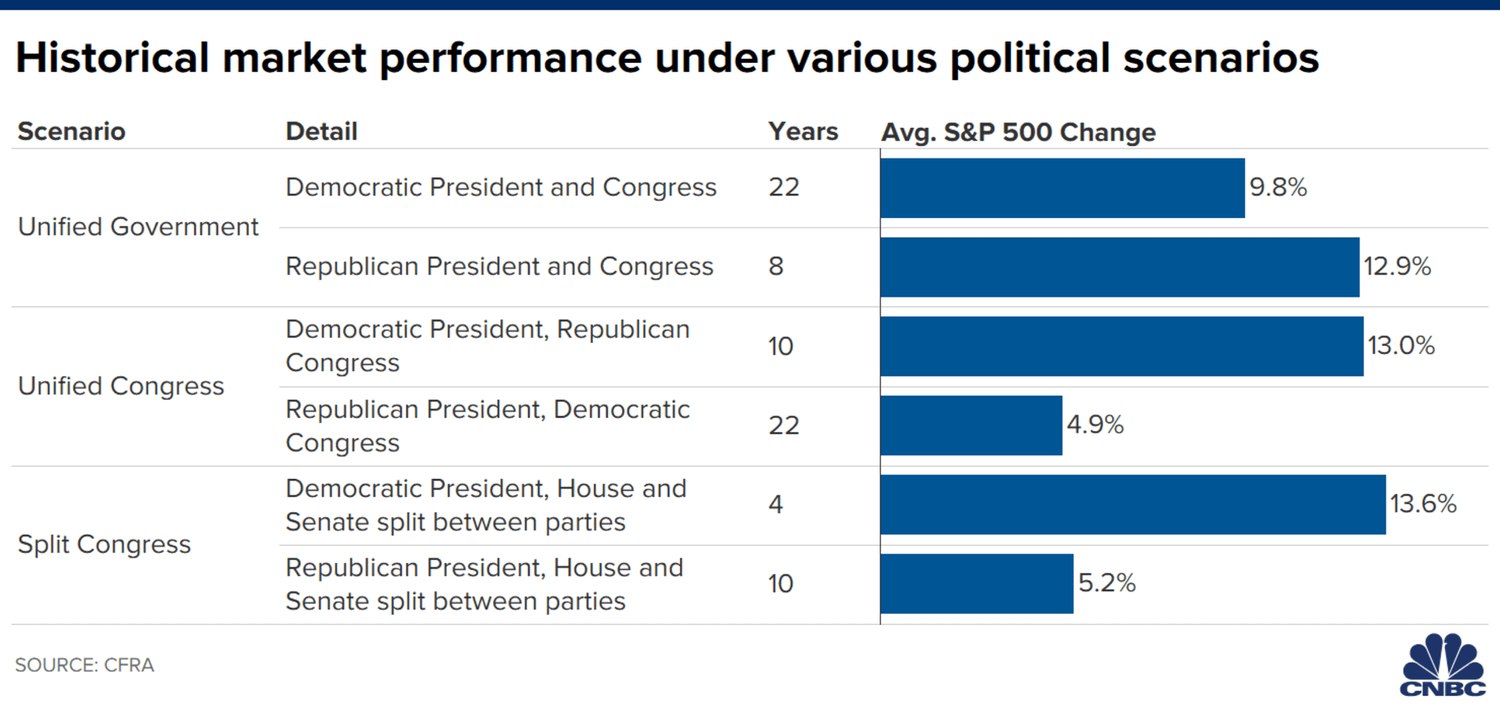

For investors worried about how a Democratic President and a Democratic Congress will impact their portfolios over the long haul, fear not: history shows that stocks usually do well regardless of which party controls the White House or Congress.

Of all the possible combinations outlined in the chart below, stocks appear to perform best when a Democrat is in the White House and Congress is split. The second-highest returns happen when a Democrat is president and Republicans control Congress.

The first year of an administration is when the new president tends to make the biggest policy proposals. Think health care with President Obama and tax cuts with President Trump. Obviously, President Biden’s first major goal is to address the pandemic. After that, it’s up in the air. Maybe he’ll try to jumpstart the economy with an infrastructure package. It seems doubtful he’d try to raise taxes with the economy in a hole, but more environmental regulations—many of which he can enact with the stroke of a pen—seem pretty certain.

On the whole, the stock market is driven the most by Federal Reserve policy changes. That’s the thing to keep your eye on.

3. More Stimulus

The global economy rebounded in 3Q 2020, primarily driven by supportive fiscal and monetary policies. The Federal Reserve has committed to keeping interest rates “lower for longer” and additional stimulus checks are “in the mail,”– both of which are market supportive.

The CARES Act paid up to $1,200 for each qualifying person, but the new COVID relief package will pay half that – up to $600 for qualifying individuals. House Democrats voted on December 28 to raise the second stimulus payment up to $2,000, but Senate Republicans blocked the vote, effectively killing the increase.

However, with a Senate that divided 50-50 between Democrats and Republicans, and Vice President-elect Harris could cast a tie-breaking vote in favor of a $2,000 second stimulus check increase. President-elect Joe Biden presented on January 14 a new $1.9 trillion coronavirus relief package that includes a third round of stimulus payments up to $1,400.

Even if the current stimulus package isn’t expanded beyond the $600, the message is clear – the government is ready to step in to support individuals and bolster the economy.

4. Search for Yield

Company earnings are a key driver of the stock market.

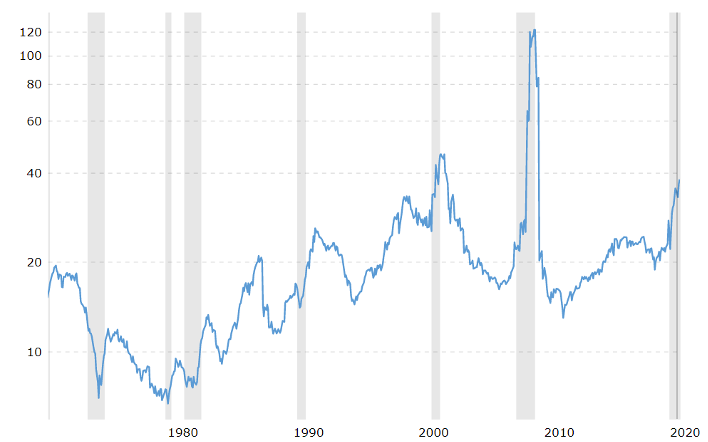

Research firm FactSet predicts the overall calendar year 2020 earnings per share (EPS) to have fallen a steep 13.6%. If that’s even close, it would be among the worst years on record, and the second year in a row of falling earnings for big companies.

The Price-to-Earnings (P/E) ratio of the S&P 500 Index tells a scary story (see chart below), nearing levels not seen since 2000. This indicates a stock market that is very overvalued, with prices (P) significantly outstripping earnings (E).

However, analysts are predicting a rebound in this year’s earnings, with research firm CFRA Research projecting 20.3% earnings per share growth for companies in the S&P 500. If this is the case, then-current P/E ratio should adjust accordingly, with earnings (E) catching up with price (P).

In spite of these lofty prices, given current historical low-interest rate levels, equities will likely continue to be the best game in town to beat inflation and provide some degree of income. So, if we get a correction, I would see this as a buying opportunity, not a reason to reduce equity exposure.

The chart below illustrates the P/E ratio of the S&P 500 Index over the past 20 years. (Source: MacroTrends.net – S&P 500 Index: 20 Year Historical P/E Ratio)

5. ESG Investing

As a money manager who has been screening the investments in our proprietary portfolios through the Environmental, Social, Governance (ESG) lens almost since our start, we are thrilled to see “ESG” becoming a household term.

Sustainability funds were experiencing big growth before coronavirus: assets doubled over the past three years, according to a new Morningstar report. But companies that rate highly on environmental, social, and governance (ESG) factors received a boost during Covid-19, with increased interest in stakeholder capitalism.

The Sierra Club Portfolio GAA that we offer to our clients experienced just over 100%+ return in 2020, with its emphasis on investing in future-focused companies like Tesla and Vestas Wind Systems. (I have to remind our readers that past performance is never a guarantee of future results!)

We anticipate that ESG will be a defining acronym of the next decade, and likely to dominate financial markets for the foreseeable future. If you want to learn more about our approach to sustainable, responsible investing, don’t hesitate to contact us.

6. Emerging Markets

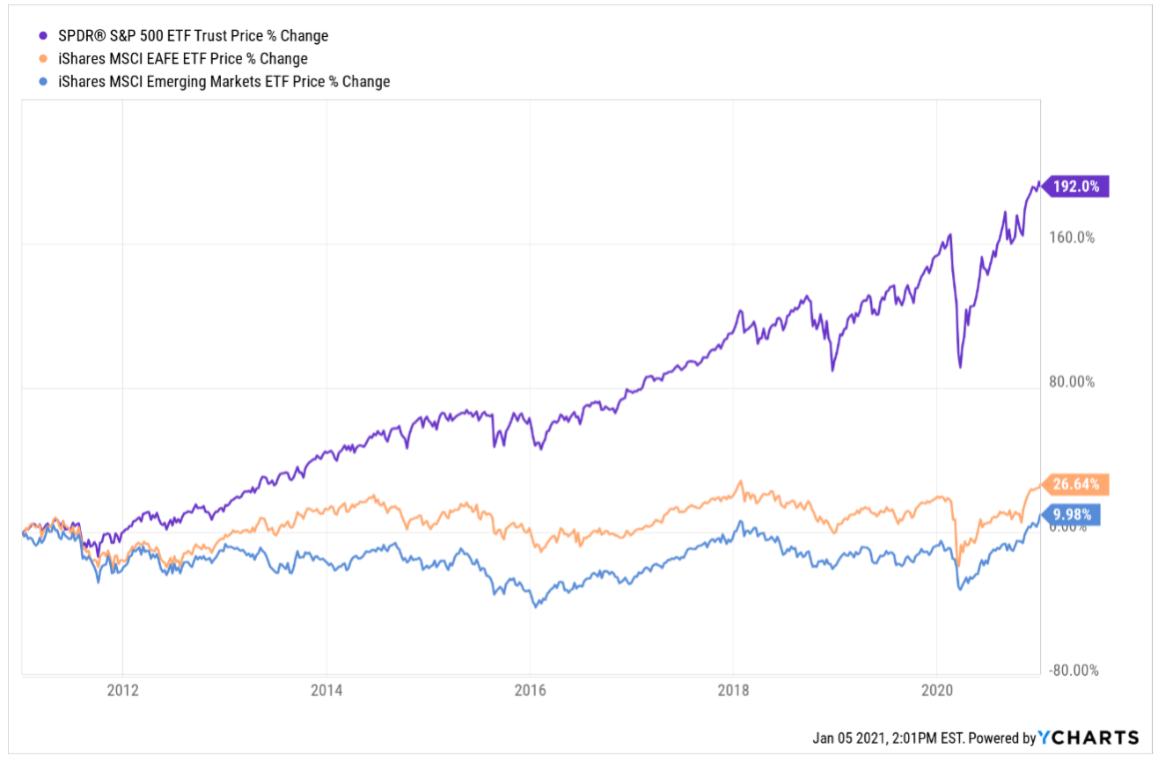

Asia has emerged as an investment spotlight with China and Emerging Markets becoming a relatively attractive opportunity.

As you can see in the chart below, for the last 10 years, US equities (SPY ETF [S&P 500 Index], purple line) have handily outperformed non-U.S. markets. We are waiting to see if international equities (EFA ETF [EAFE Index], orange line) and emerging equity markets (EEM ETF blue line) can push above their 2018 peak before making any commitments. But we would not be surprised if international equities performed fairly well this year assuming a continued weaker US dollar and the relative valuations.

While we think the market is likely due for a breather, we believe the wind is likely at the market’s back – at least for a few more months – barring increased civil unrest or a big spike in the U.S. dollar.

Give us a call or send us an email if we can assist as you plan for 2021.