Feeling the heat? Summer is here. Higher temperatures are here to stay for the next few months.

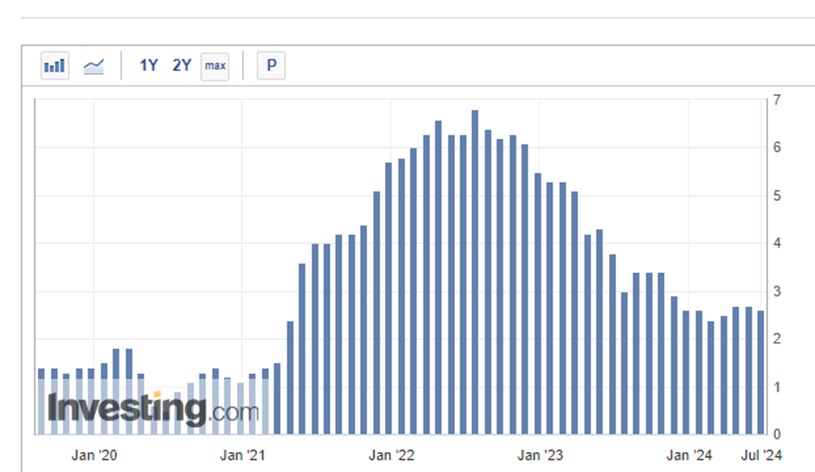

Inflation has been having its own heat wave for the past few years. We’ve seen the numbers climbing, with the Consumer Price Index (CPI), a key inflation gauge, peaking at 8.0% in 2022.

When will the inflation heat wave break? What are the key things to know?

- CPI Drop: Believe it or not, the Consumer Price Index has already dropped by over half since peaking, with its most recent reading in June at 3.4%*. This is good news as it tells us the Federal Reserve’s policy of raising interest rates to quell inflation is working.

- Grocery and Dining Costs: You might be asking, “If CPI has been cut in half, why am I still leaving the grocery store and restaurant feeling so much poorer than I did a few years ago?” According to NerdWallet, despite the CPI coming down, the index for food at home is 1.1% higher than a year ago and dining out costs have increased approximately 4.1%. What is going on? Inflation doesn’t impact things evenly, and food prices are some of the most volatile – they can stay higher for longer. Also, food pricing is complicated – prices are impacted by all sorts of factors such as supply-chain disruptions and tariffs on imports. For example, you probably don’t spend time thinking about where your bread or corn chips are sourced. If you did, you would know that exports from Ukraine have historically accounted for 9% of the global wheat market and 12% of the corn market according to the USDA’s Foreign Agricultural Service!

- Housing Market Impact: Inflation has been good for the housing market – if you own your home. According to Zillow data, the national average home price in the U.S. has climbed 29% since the COVID-19 pandemic began in 2020. But for those looking to buy a home, the current environment has been extraordinarily challenging. Not only have prices soared, but higher interest rates have meant that mortgage payments have also gone up, pricing many out of homeownership.

- Mortgage Rates: If inflation has come down, why haven’t mortgage rates dropped? The 30-year mortgage rate peaked at just over 8% in the fall of 2023 and as of July 2, is not far off this level, hovering around 7.1%.** Mortgage rates are a byproduct of the Federal Reserve’s interest rate policy. The current federal funds rate, which is the rate set by the Fed and upon which other rates (including mortgage rates) hinge, is currently 5.25%–5.50%. This rate was set in late July 2023 and has remained unchanged since.

- Future of Inflation and Interest Rates: When will inflation and interest rates come down? Mortgage rates have remained high because the underlying economic factors – sticky inflation, full employment, and consumer spending – have not aligned in a way that would prompt the Federal Reserve to lower rates. Until the Fed sees a path to lower interest rates, mortgage rates will remain near current levels.

It’s important to remember the economy (and the stock market) is cyclical. The cycle will have a beginning and an end. Since World War II, there have been six periods in which the CPI was 5 percent or higher. Most of these cycles lasted less than 2 years – except for the period from April 1973 to October 1982, when the United States was dealing with high inflation due to two dramatic surges in oil prices.

Right now, we are in one of these cycles – and it’s uncertain when this will end. As of their June meeting, the Federal Reserve continues to be in a wait-and-see mode – to see an increase in unemployment, signaling that the economy needs to be stimulated by lower interest rates. Prior to the June meeting, the projections were for three interest rate cuts in 2024. As of the June meeting, this has been reduced to just one cut. Additionally, the upcoming presidential election has significant implications. Trump has clearly stated his plans to increased tariffs and apply more isolationist policies, both of which could have a profound impact on the economy – and result in higher inflation.

One thing is for sure, we aren’t going back to the “nickel loaf of bread.”

* Investor.com

** MortgageNewsDaily.com

About the Author

Roberta Keller

Roberta is passionate about the intersection of money and social impact. Her goal has been to build a business that integrates her institutional money management experience with her yoga and meditation practices.